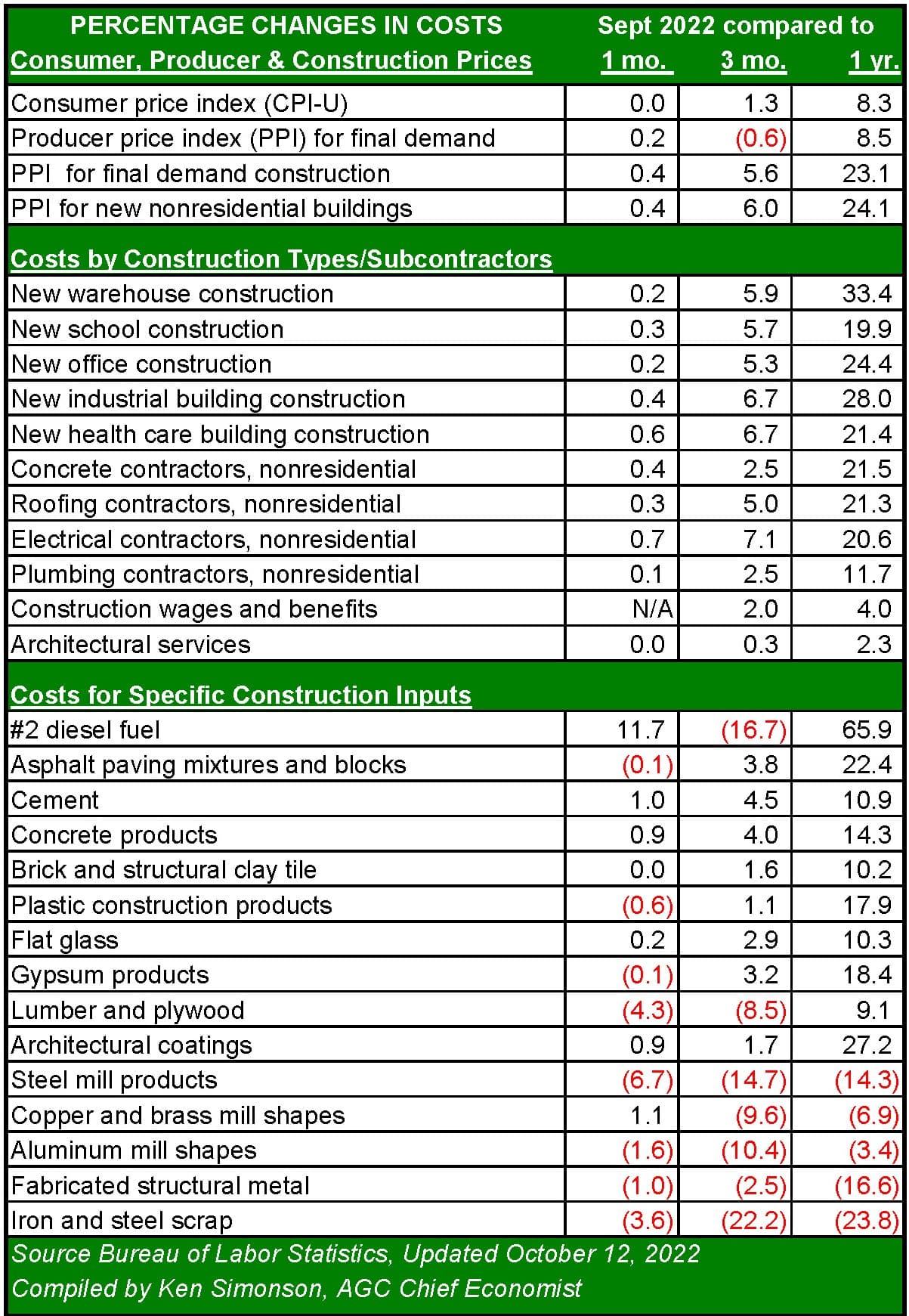

The October 12 report on inflation from the Bureau of Labor Statistics (BLS) showed a flattening of producer prices over the past 30-90 days, which may indicate that price increases have peaked. But the rate of inflation compared to September 2021 remains elevated and, for construction, is nearly four times the rate of producer prices overall.

Producer price indexes (PPI) fell for construction metals and some products associated most closely with residential construction. That pushed the PPI for inputs used in nonresidential construction down 0.2 percent compared to August 2021; however, the change in PPI for nonresidential construction inputs from one year earlier was 12.8 percent, or more than four percentage points higher than the PPI for final demand overall. Moreover, inflation for nonresidential building construction, which includes the costs of labor and other contractor costs, rose to 24.1 percent year-over-year.

The decline in energy prices and global demand pushed steel, aluminum, and copper prices significantly lower compared to 90 days earlier. There was a 22.2 percent decline in the price of iron and steel scrap. The price of #2 diesel was also down significantly compared to June 2022, but a double-digit increase in diesel since August represents a threat to construction costs because projects require hundreds (or thousands) of truck deliveries of materials and equipment.

Even with the recent dip in some materials, prices of several widely used commodities posted double-digit increases over the past 12 months. The index for liquid asphalt was 43.3 percent higher, despite an 11.8 percent decline from August to September. The PPI for architectural coatings rose 27.2 percent over the previous 12 months. There were also double-digit year-over-year increases in the price indexes for materials used heavily in residential construction, such as drywall, which rose 18.4 percent, plastic construction products (17.9 percent), asphalt roofing materials (15.3 percent), concrete products (14.3 percent), insulation (13.4 percent), and flat glass (10.3 percent).

September’s stubbornly high consumer inflation will add to the pressure on the Federal Reserve Bank to maintain restrictive interest rates through 2023. The markets are betting that inflation will respond to that pressure by mid-2023. However, the lagged relationship between producer prices and construction put in place means that ongoing projects will continue to see costs that are 20 percent higher than in 2021 until spring 2023 or later. The BLS report found that the PPI for five major nonresidential building types – warehouses, schools, offices, industrial, and healthcare facilities – averaged more than 25 percent higher year-over-year. The PPI for warehouses was 33.4 percent higher year-over-year. Likewise, the increase in PPI for four types of specialty contractors – concrete, roofing, electrical, and plumbing – increased by an average of almost 9 percent. The latter reflects the bid prices from contractors, which historically lag increases in inflation by 12 to 18 months. Bid prices will remain elevated until disinflation trends for an extended period and margins begin to recover.