Article written by:

Rebekah Smith, CPA, CFF, CVA, MAFF

Director of Forensic and Dispute Advisory Services

With the changes to the Paycheck Protection Program (“PPP”) made by the Paycheck Protection Program Flexibility Act of 2020 (“Flexibility Act”), many companies are now contemplating whether the original eight-week period or the newly available 24-week period will be better for their forgiveness.

With questions about the changes still outstanding, and anticipated, revised application plus the end (or pending end) of many eight-week periods, is making decisions very difficult without relevant information.

Key Questions

One of the key questions is whether you have to go the full 24 weeks, or can you stop when you “run out” of PPP monies? Currently, that answer seems clear; the amendments to the CARES Act basically replaced the eight weeks with 24 weeks, and so it seems to be a choice – either eight weeks or 24 weeks. While a business might run out of money before the 24 weeks is up, for example in week 12, it would seem that the business has to keep tracking full-time equivalent employees (“FTEE”) for the entire 24-week period.

The Flexibility Act also replaced all CARES Act references to “June 30, 2020” with “December 31, 2020” which includes the “safe harbor” date to return to specified levels of employment. This safe harbor date now appears to be December 31, 2020. What does this mean for borrowers who opt for the eight-week forgiveness period? If they need to use the safe harbor to achieve 100% forgiveness, do they need to wait until the end of the year? For companies who have been making hiring and firing decisions based on an eight-week period and the June 30, 2020 date, these questions are critical.

The other critical question is, what amount will the FTE reduction percentage be applied to – the total spent during the 24 weeks, or will it be capped at the amount of the loan? The current loan forgiveness application multiplies the total spent by the FTEE reduction percentage, however with the total spent increasing over the longer period that approach will render the FTEE reduction percentage irrelevant for many companies because the resulting amount will still be more than the PPP loan.

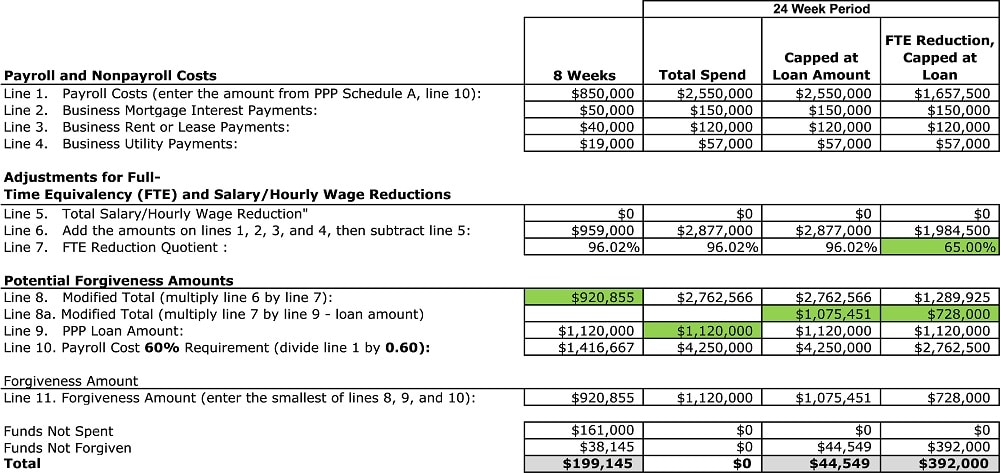

The Math

The below example demonstrates how answers to these questions could impact the total that has to be repaid or returned to the bank and the importance of understanding the potential implications. Below we have set forth:

- Eight Weeks – Depicts the original eight-week period which left the business with $161,000 not spent and $38,145 not forgiven (due to an FTE reduction) for a total of $199,145 that would need to be repaid.

- 24 Weeks Applied to Total Spend – This scenario assumes that spend and FTEEs would be similar in the 24-week period as they would in the eight-week period and that the FTEE percentage will be applied to the total spend. As can be seen below, all monies will be spent and there will be 100% forgiveness.

- 24 Weeks Applied to Total Loan Amount – This scenario assumes that spend and FTEEs would be similar in the 24-week period as they would in the eight-week period and that spend is capped at the loan amount. As can be seen below, all monies will be spent; however, the forgiveness will be limited due to the FTEE percentage reduction with the company owing $44,549.

- 24 Weeks, FTEE Reductions, Applied to Loan Amount – This scenario shows reduced spending and FTEE reductions, as well as assuming that the spend will be capped at the loan amount. As can be seen, the company is worse off for having gone the 24 weeks in this scenario and will owe $392,000.

|

While the unforgiven amount between the eight weeks and the 24 weeks capped at the loan amount increased (going from $38,145 to $44,549), the overall total dollars that have to be paid back by the company went down (from $199,145 to $44,549). By using the 24-week period, the company was able to use more of the PPP monies to fund expenses they would have incurred anyway. In fact, until the retention percentage drops below approximately 83%, it will still be more beneficial to use the 24-week period since 83% of the loan amount ($1,120,000 * 83% = $929,600) is greater than the amount of forgiveness ($920,855) under the eight-week scenario.

Qualitative Considerations

As accountants, we sometimes look at things as a “math” problem, but as business advisors, we have to recognize that there are often business issues that might drive the decision as well.

- Waiting for 16 additional weeks may result in too much focus on PPP management and less focus on running the business in the most effective manner. Having to continue to manage FTEEs may prove burdensome and cost more in the long run.

- Several business owners we have spoken with tout the benefit of an eight-week period in that the PPP loan will be complete and resolved all in one year. Extending to the 24 weeks could lead to the forgiveness process extending into 2021.

- The new safe harbor date is now December 31, 2020. If a business needs to use the safe harbor date in order to achieve 100% forgiveness, it would appear that waiting until December 31, 2020, is the only option (pending additional guidance on this issue). For some, the uncertainty of waiting for the safe harbor date is unattractive and the preference is to take less forgiveness in order to be done sooner.

As you have probably come to expect with the PPP, more guidance – and a revised forgiveness application form – is expected with the hope of clarifying some of the open questions discussed above. Until then, we encourage companies to continue to make sound business decisions while monitoring their payroll and headcount to maximize the use and potential forgiveness of its PPP loan. Our SBA team is available to help companies work through various scenarios (as demonstrated above) in order to help maximize potential PPP loan forgiveness. If you have any questions about the eight-verses 24-weeks options for your company, please contact a member of GBQ’s SBA team – Rebekah Smith, Dustin Minton, or Jeremy Bronson.