Summary

On June 6, 2016, Connecticut Governor Dannel P. Malloy (D) signed into law S.B. 502, 2016 Gen. Assem., May Spec. Sess. (Conn. 2016), which adopts single sales factor apportionment for Personal Income Tax purposes, and market sourcing for Corporation and Personal Income Tax purposes. These provisions in S.B. 502 apply to taxable years beginning on or after January 1, 2016, for Corporation Income Tax purposes and taxable years beginning on or after January 1, 2017, for Personal Income Tax purposes.

Details

Single Sales Factor Apportionment

For taxable years beginning on or after January 1, 2017, under the Personal Income Tax, Connecticut apportions items of income, gain, loss, and deduction attributable to a business, trade, profession, or occupation carried on in the state via a single sales factor. This provision applies to the income of a nonresident individual, including a nonresident partner’s, shareholder’s, and beneficiary’s share of income.

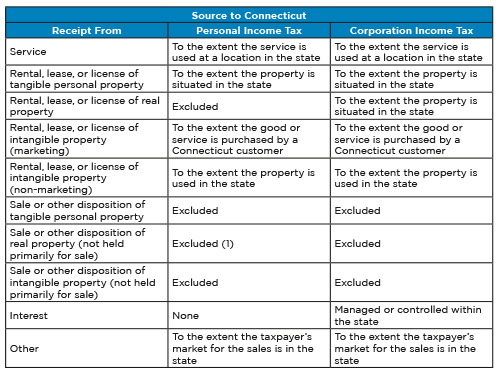

Market Sourcing for Apportionment

For taxable years beginning on or after January 1, 2016, for Corporation Income Tax purposes and for taxable years beginning on or after January 1, 2017, for Personal Income Tax purposes, Connecticut adopts the following framework for assigning receipts from sales of other than tangible personal property held primarily for sale. For Personal Income Tax purposes, these provisions also apply to the income of a nonresident individual, including a nonresident partner’s, shareholder’s, and beneficiary’s share of income.

(1) All sales of real estate are excluded under the Personal Income Tax.

A taxpayer that cannot reasonably determine the assignment of receipts under the foregoing rules may petition the Commissioner of Revenue for approval of a methodology that reasonably approximates the assignment of such receipts. Connecticut requires the taxpayer to file the petition within 60 days prior to the original due date for the first return to which the petition applies. The Commissioner is required to grant or deny the petition before the original due date for the return.

Insights

- Connecticut’s adoption of single sales factor apportionment for Personal Income Tax purposes aligns the apportionment of income under that tax with the apportionment of income under the Corporation Income Tax, at least with respect to taxable years beginning on or after January 1, 2017. Connecticut adopted single sales factor apportionment for Corporation Income Tax purposes in December 2015, which applies to taxable years beginning on or after January 1, 2016.

- Connecticut’s adoption of market sourcing was expected given that most, if not all, states that have adopted single sales factor apportionment have also adopted market sourcing at the same time or shortly thereafter.

- Since the new law was enacted on June 6, 2016, Connecticut taxpayers should assess what, if any, impact these law changes may have on their existing deferred tax balances, and adjust accordingly as of the enactment date.

- We anticipate that the Department of Revenue Services, like other states that have adopted market sourcing, will need to issue further administrative guidance regarding its interpretation for determining “the extent the service is used at a location” in Connecticut.

This article originally appeared in BDO USA, LLP’s State and Local Tax Alert – July 2016. Copyright © 2016 BDO USA, LLP. All rights reserved. www.bdo.com.