Article written by:

Joseph Borowski, CFA

Director, Valuation & Financial Opinion Services

2020 has been a challenging year for many individuals who have seen their jobs eliminated, retirement accounts reduced, and/or their health threatened. Many restaurant owners have experienced mandated capacity restrictions limiting sales, disrupted supply chains, and difficult decisions regarding their workforce. At the same time, challenges often create opportunities, and this environment has created a unique opportunity for restaurant owners to transition wealth to the next generation in a tax-efficient manner.

Lower Company Values

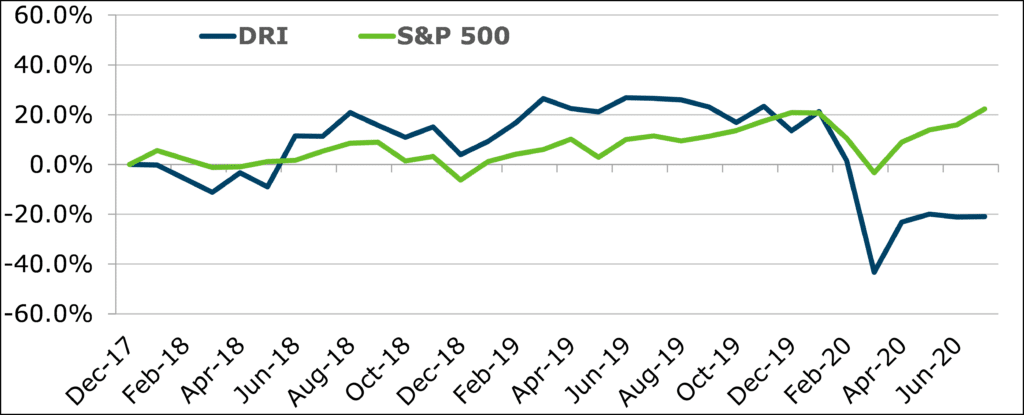

A restaurant’s value is tied to its expected future cash flows, which provide a return to investors. Due to the pandemic and its impact on the economy, companies in most industries, and perhaps especially those in the restaurant industry, have seen expected cash flows fall, and the risks to those cash flows rise. Customer traffic is down, and there is great uncertainty on when conditions will return to normal. Further, months of net losses may have weakened restaurants’ balance sheets, further reducing values. Using the public markets to highlight this concept, the stock price for Darden Restaurants’ (which owns and operates restaurants under the Olive Garden, LongHorn Steakhouse, and other brand names; NYSE: DRI) fell over 30% between January and July 2020, per the chart below, due to falling revenue/profit and uncertainty about when conditions will return to normal.

While lower values may make restaurant owners less interested in selling their business in the near-term, lower values are attractive to those who instead wish to gift equity in their business to family or others (either permanently, or in advance of a future sale). That is because wealth transfers above a specific level, known as the estate tax lifetime exemption, are subject to estate taxes.

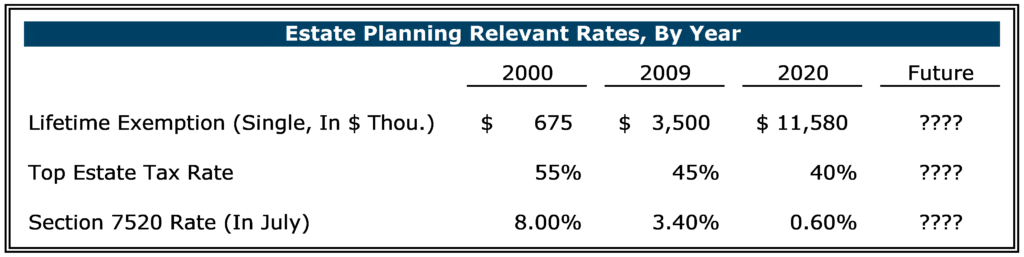

Favorable Exemption and Rates

Below are common variables that impact estate taxes on wealth transfers:

- Estate Tax Exemption – The value of an estate that can be transferred to heirs before estate taxes become due

- Estate Tax Rate – the applicable tax rate for wealth transfers above the lifetime exemption

- Section 7520 Rate – the applicable interest rate used in grantor retained annuity trusts (GRATs), a popular financial instrument in estate planning. A lower Section 7520 rate makes this instrument more attractive.

As shown in the table below, these variables are all currently at extremely favorable levels relative to prior years. At the same time, there is no guarantee that this will continue in the future, especially with an upcoming election later in 2020. History tells us that these rates can be changed fairly quickly, including after a change in control of the U.S. presidency and houses of Congress.

Company Values Can Improve Quickly

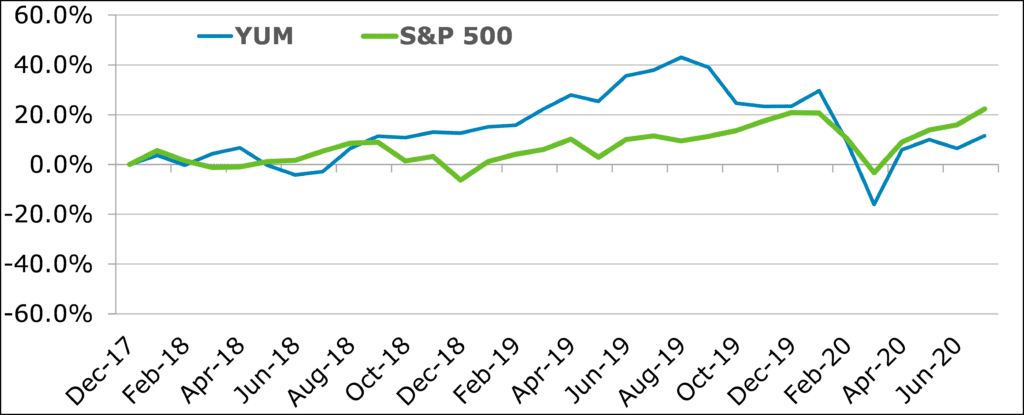

Not all industries have been adversely impacted by the pandemic, and some have been positively affected. Even within the restaurant industry, some fast food chains with strong drive-thru/carryout volume have performed comparably well in 2020. Again, using the public markets for example, YUM! Brands, Inc. (which operates KFC, Pizza Hut, and Taco Bell restaurants worldwide; NYSE: YUM), has seen its equity value recover quickly per the following graph (down less than 10% in 2020 through July; up 33% since March) as cash flow and outlook has improved.

In this unusual environment, conditions can change quickly. Once a company’s future outlook improves, its value can increase rapidly. This creates urgency for restaurant owners to act now while customer traffic is down and values are still impaired.

Consult with Professionals

Before making any decisions, remember to consult with your professional advisors – attorney, accountant, and valuation professional. There are several options and vehicles available to transition wealth, and these individuals can ensure your wealth transfer strategy meets your estate planning goals (and minimizes associated estate taxes). For example, when transferring equity in a privately-held business, it is ideal to transfer non-controlling equity interests, since the value of these interests can be discounted from their pro-rata value.

Conclusion

Lower restaurant values, combined with favorable estate tax exemption and rates, make now an ideal time for most restaurant owners looking to transition wealth. At the same time, economic outlook and business values can change rapidly which encourages action now. To learn whether the value of your restaurant business has decreased, and if the timing is right to transition wealth to the next generation, please contact Joe Borowski.

For more information and insights, we are pleased to provide access to our “Lower Company Values Create Estate Planning Opportunity” webinar recording.