Article originally published December 1, 2021

Last updated April 6, 2022

Update: Federal guidelines have been clarified since the publishing of this article. Funds expended through the Restaurant Revitalization Fund are not subject to single audit requirements. As a result, these funds should not be accumulated in determining the total funds expended for single audit determination. Economic Injury Disaster Loan expenditures are subject to single audit requirements if certain thresholds are met and the information in this article applies to this funding stream.

The restaurant industry has been hit hard by the COVID-19 pandemic resulting in capacity limitations, business closures, regulatory mandates and restrictions and significant labor constraints. These negative pandemic effects have been partially mitigated through many avenues of federal funding including, but not limited to, the Paycheck Protection Program (PPP), Restaurant Revitalization Fund, Economic Injury Disaster Loans (EIDL) and Employer Retention Tax Credits (ERC). Traditionally federal funding was likened to a nonprofit organization and something that most likely was never considered before by restaurants. But what must be considered now, is whether these sources of federal funding could result in an organization being subject to a Single Audit.

What is a Single Audit?

A Single Audit is a financial statement and federal awards audit for any organization that expends $750,000 or more in federal funds in one year. A Single Audit requires 1) an audit of the financial statements along with 2) an audit of what are considered “major federal programs” in accordance with the Uniform Guidance issued by the Office of Management and Budget (OMB). As this is a governmental requirement, the audit of the financial statements is more cumbersome than what would typically be incurred under Generally Accepted Auditing Standards. The Single Audit is performed in accordance with Governmental Auditing Standards, which requires additional audit reports on internal control over financial reporting and on compliance with major program requirements. If your organization does not currently complete an audit, or only has an annual review performed, the scope of the engagement will need to increase to an audit to satisfy Single Audit requirements. As a result, the aspect of a Single Audit could have far-reaching time and effort consequences for many organizations.

What entities and organizations need to complete a Single Audit?

The short answer is any organization that expends more than $750,000 in federal funds in their audit period is then required to have a Single Audit performed. Some relief has been granted by the OMB regarding certain federal funding programs. For example, expenditures associated with PPP loans, traditional SBA 7(a) loans, as well as ERC funds expended, are not included within total expenditures for the period in determining Single Audit eligibility. However, Restaurant Revitalization Funds expended as well as Economic Injury Disaster Loans (EIDL) are not excluded from the guidance. As a result, if your organization received and expended more than $750,000 in Restaurant Revitalization Funds, EIDL funds, or a combination of the two during the current or most recent period then you will be required to have a Single Audit completed.

A key point to also note is that per Governmental Auditing Standards, the audit must cover the entire operations of the auditee. In other words, all entities, units, locations, etc. in a group that meet the requirements for consolidation in accordance with Generally Accepted Accounting Principles would be required to be included. Thus, if individual entities have less than $750,000 in applicable federal expenditures but the consolidated total is greater than $750,000, the Single Audit would be required.

What are the deadlines for completion of the Single Audit?

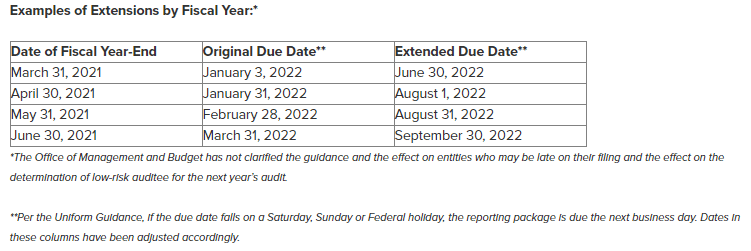

The historical deadlines for completion of a Single Audit have been nine months after the end of your reporting year, regardless of whether that is a calendar or fiscal year. However, additional relief has been granted in this regard as well, and currently, any organization with a reporting year-end of June 30, 2021, or prior has a six-month extension to complete and file their audit results with the Federal Audit Clearinghouse (FAC). See below for current examples of the extension period.

The due dates have not been extended for any years ended after June 30, 2021, at this time and thus the due date for organizations with a year-end of December 31, 2021, would be September 30, 2022. To the extent that extensions are provided in the future, we will report on them as soon as we have the pertinent information. An additional note is that if the audit is completed before the deadlines specified, the results of the audit still have to be submitted to the FAC within 30 days of the date of the auditor’s report.

We anticipate that there will be many organizations that will be required to undergo a Single Audit for the first, and perhaps only, time. This will require an increase in both time and effort as well as compliance with complex governmental requirements so we recommend that you determine if your organization will need a Single Audit sooner rather than later. If you have any questions on the eligibility of your organization or any other applicable matters please reach out to the GBQ Restaurant Team.

Article written by:

Tobin Perrill, CPA

Senior Manager, Assurance & Business Advisory Services