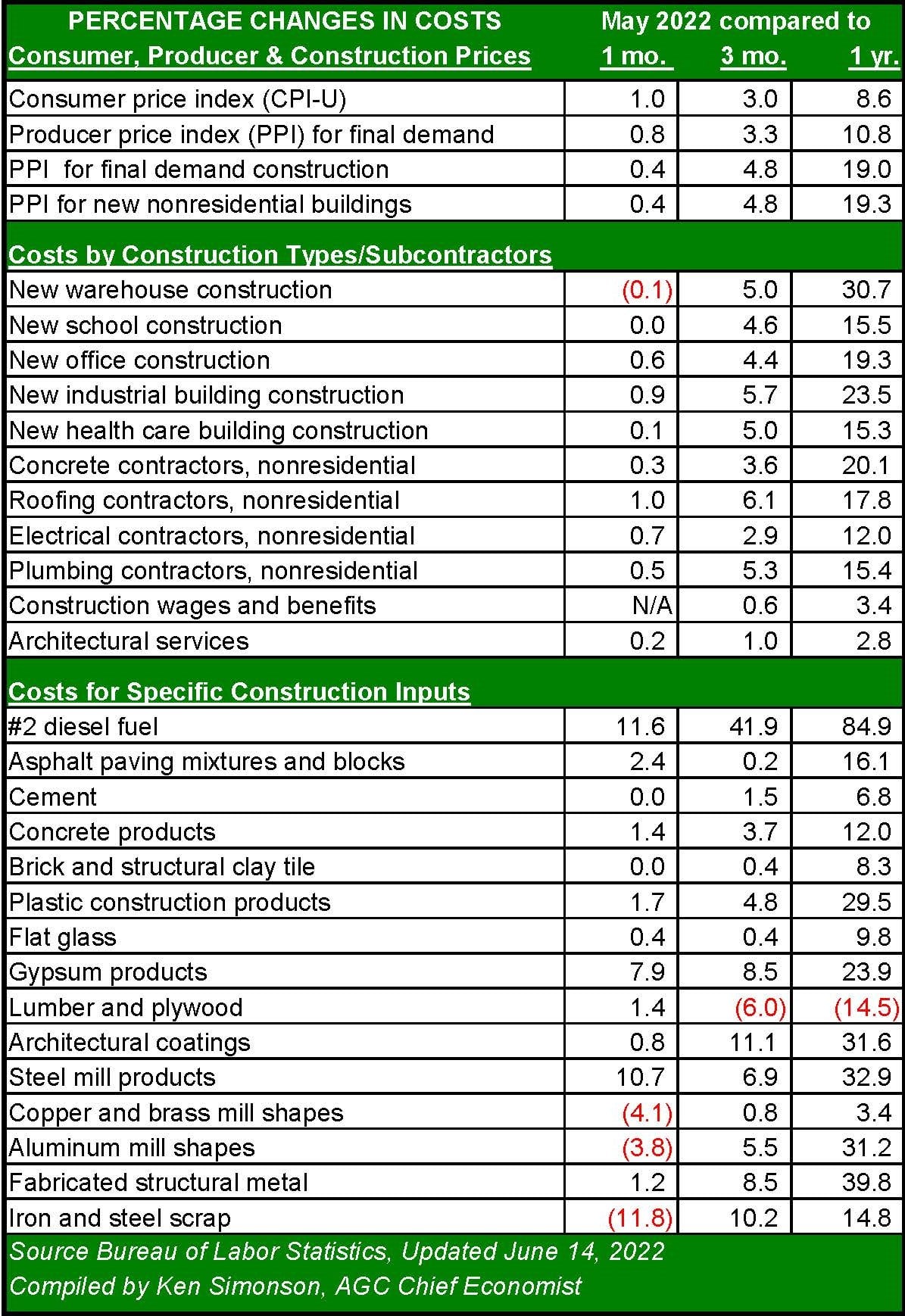

The June 14 report on producer price inflation mirrored what has been reported on consumer inflation over the past 60 days. Year-over-year inflation remains extremely high for producers; however, the rate of inflation has stopped increasing and has eased slightly. During the run up in construction inflation over the past 15 months, the rate of inflation has paused for two or three months on three separate occasions, only to soar higher. As the government and central banks turn their full attention to reeling inflation back to the long-term trend, the unanswered question is whether this latest pause is the turning point in construction cost escalation or merely another launching point.

The producer price index (PPI) for new nonresidential buildings was up 0.4 percent from April to May and 19.3 percent year-over-year, according to the Bureau of Labor Statistics. The May pace of inflation was 3.7 percentage points lower than in the previous month, a significant change in direction. The biggest increases from April to May were related to the oil price. Energy inputs to construction was 10.6 higher, as was the price of #2 diesel fuel, which was 84.9 percent higher year-over-year. There were notable declines in the industrial metals. Copper and brass mill shapes fell 4.1 percent, while aluminum mill shapes declined 3.8 percent. Prices for scrap metals fell steeply, with iron and steel scrap dropping 11.8 percent and stainless steel falling 13.1 percent. Steel mill products saw a 10.7 percent increase, however, after cooling for several months.

The context for these data points is important in mid-2022. There are several trends worth watching for those looking for signals about construction inflation over the remainder of 2022.

- May’s producer price inflation reflects little or no impact of the monetary policy actions taken by the Fed since March. Changes in producer price trends reflect changes in supply chain and/or perceived changes in future demand. In May, the supply chain remained disrupted and demand for construction materials had not cooled.

- While the construction workforce remained in short supply, which put more upward pressure on wages than in the overall labor market, wage pressures in the larger economy eased through May. As reported in the May Employment Situation Summary, wages increased at a 5.2 percent clip year-over-year, but only 0.3 percent compared to April. Moreover, the three-month rate of increase declined from six percent earlier in 2022 to 4.5 percent in May.

- Core inflation eased in April, following the first decline in March. Core inflation is the measure preferred by the Fed because the spending data comes from businesses, and it provides a better gauge of how consumers are moderating demand for a broader base of items. The main drivers of inflation, food and energy prices, remain elevated; however, the decline in core inflation suggests that consumers have begun to respond.

These are merely early indicators of a potential change in direction, not a change in the trend. Construction costs will not retrench to “new normal” levels until a fully functioning global supply chain is restored, but the latest readings on inflation offer the first signs that the pace of inflation is responding to the Federal Reserve Bank’s interventions. The slowdown in wage growth is an important indicator, as it suggests that the perception of continuing inflation has not yet become baked in. And the fact that there are signs of changes in consumer behavior increases the potential for inflation to cool while the supply chain re-balances in 2023.